Key Takeaways

- Surety bonds are not insurance. They protect the public, not the business owner.

- Licensing often requires bonding. Skipping this step can stop your startup before it begins.

- Bonding builds credibility. Customers prefer businesses that are licensed and bonded.

- Costs vary. Expect to pay 1–3% of the bond’s value, higher if credit is poor.

- Optional bonds add value. Even if not required, they can set your startup apart.

- Digital healthcare providers, contractors, and service businesses especially benefit from advertising their bonding status to increase trust.

Launching a startup is exciting. You’re brimming with ideas, drafting business plans, talking to potential customers, and perhaps even designing your website or storefront. But amid the rush, there’s one detail that too many entrepreneurs overlook: surety bonds.

For small service-oriented businesses—think plumbing, cleaning, or landscaping—the question often arises: Do I really need to be bonded? Isn’t insurance enough?

To tackle this, I spoke with Kevin Kaiser, a small business compliance expert at nationwide bonding agency SuretyBonds.com, who explained what surety bonds are, why they matter, and how they can make or break your startup’s credibility.

This guide dives deep into surety bonds, from their role in consumer protection to how startups can leverage them for growth. We’ll also explore expert insights, real-world examples, and actionable tips you can apply to your own entrepreneurial journey.

Table of Contents

What Exactly Is a Surety Bond?

At first glance, a surety bond might look like just another form of insurance. But in reality, it’s a completely different tool.

A surety bond is a three-party agreement:

- Principal – That’s you, the business owner or service provider.

- Obligee – Usually a government agency, client, or entity requiring the bond.

- Surety – The company that issues the bond and guarantees compensation if the principal fails to meet obligations.

In short, a surety bond guarantees that your business will follow laws, regulations, or contractual agreements. If you don’t, the affected party can file a claim, and the surety company steps in to provide compensation.

Kevin Kaiser explains it this way:

“Think of a surety bond as a promise with teeth. It’s not just you telling your customers you’ll deliver—it’s a binding agreement backed by a third party that ensures accountability.”

What Surety Bonds Do

In essence, surety bonds guarantee that work will be performed according to a contract or to all applicable laws and regulations. If a business fails to fulfill its duty or legal obligation, then the injured party can file a claim against the bond and receive some type of compensation. For example, notary publics in all 50 states must obtain a notary bond before receiving their license. If they abuse their office or somehow harm a consumer, that individual can fail a bond claim and expect to receive appropriate compensation. The surety company that issued the bond is there to ensure the problem is made right.

Many consumers avoid small businesses and home-based companies that lack proper bonding – without it, there’s no guarantee their interests will be protected. A host of other business types either require surety bonds or are excellent candidates. Here’s a look at a few:

- Real Estate Brokers

- Collection Agencies

- Durable Medical Equipment Providers

- Health Clubs

- Auctioneers

- Travel Agencies

- Notary Public

But small businesses can also benefit from non-mandatory surety bonds. Companies with a couple employees – a small accounting firm, for example – can buy Employee Theft Bonds, which insulates them against financial harm if one of their employees steals.

Surety Bonds vs. Insurance: What’s the Difference?

It’s easy to confuse surety bonds with insurance, but the two serve very different purposes:

- Insurance protects your business from risk. For example, liability insurance covers damages if your work accidentally causes harm.

- Surety bonds protect the public or your customers. They guarantee you’ll meet legal or contractual obligations.

Here’s a practical example:

Imagine you’re a contractor hired to remodel a kitchen. If you damage the homeowner’s property, your insurance covers the cost. But if you walk away before finishing the job, the homeowner can file a claim against your surety bond for failing to meet your contractual duty.

That distinction is crucial. Insurance builds your safety net. Surety bonds build your customers’ trust.

Why Startups Should Care About Surety Bonds

1. Licensing Requirements

Many industries legally require bonding before issuing licenses. Notaries, auto dealers, collection agencies, health clubs, and construction contractors are just a few examples. Without a bond, you might not even get permission to operate.

2. Credibility with Customers

Consumers are wary of fly-by-night businesses. When your ads say “licensed and bonded,” it signals professionalism and security. For startups trying to gain trust, this can be the deciding factor in landing new clients.

3. Access to Bigger Contracts

Large projects—especially government contracts—almost always require bonds. A startup plumber might get by without a bond for residential work, but to bid on city projects, bonding is non-negotiable.

4. Protection Against Internal Risks

Some bonds, like employee theft bonds, help protect you if your staff acts dishonestly. This can be a lifesaver for small accounting or bookkeeping firms where trust is paramount.

Real-World Examples

Case Study 1: The Licensed Contractor Who Won More Jobs

A small construction startup in Michigan struggled to win contracts because it wasn’t bonded. Competitors who advertised as “licensed and bonded” easily won bids, even when their prices were higher. After securing the proper bonds, the startup began winning municipal contracts—ultimately doubling revenue in just one year.

Case Study 2: The Notary Public

Every notary in the U.S. must have a bond. In one case in California, a notary mishandled real estate documents, causing financial harm to the client. The client filed a bond claim and was compensated—saving the notary from a potentially devastating lawsuit.

Case Study 3: The Cleaning Business Startup

A home cleaning startup in Texas discovered that bonding wasn’t legally required but found that customers asked about it often. By obtaining an optional bond and advertising as “licensed, insured, and bonded,” the business saw a 40% increase in new client conversions.

How to Obtain Surety Bonds

Applying for a bond is similar to applying for a loan:

- Choose the right bond type. Different industries require different bonds (contract bonds, license bonds, fidelity bonds, etc.).

- Submit an application. You’ll need financial details, business history, and sometimes personal credit info.

- Underwriting review. Surety companies evaluate your creditworthiness, financial strength, and risk profile.

- Pay the premium. Usually 1–3% of the bond’s face value.

Pro Tip from Kevin Kaiser:

“Don’t assume bad credit disqualifies you. Specialized agencies work with high-risk applicants, though premiums may be higher. Start small, build your credit, and your bond costs will drop over time.”

Expert Tips for Startups Considering Surety Bonds

For many first-time entrepreneurs, surety bonds can feel like an unfamiliar piece of paperwork tucked into the long checklist of startup requirements. But when handled strategically, bonding can become much more than a box to tick—it can be a competitive advantage that helps your startup stand out, win trust, and scale faster. Drawing from industry best practices and insights from compliance experts, here are some key strategies to keep in mind:

1. Budget Early

Bond costs may not be the largest line item in your startup budget, but failing to plan for them can cause unnecessary delays. Licensing agencies often won’t process your application until proof of bonding is submitted. If you wait until the last minute, you risk pushing back your launch date or losing a client contract. By setting aside funds for bonding early in your planning stage—alongside insurance, permits, and other compliance expenses—you’ll avoid surprises and position yourself for a smooth start.

2. Work with Specialists

Not all insurance companies handle surety bonds, and those that do may not offer the best rates or guidance. Specialists like SuretyBonds.com work exclusively in this area, giving them a clearer understanding of industry-specific requirements and underwriting processes. This expertise can save you time and money, especially if you’re in a regulated field like contracting or healthcare where the rules are strict and often confusing. Think of bond specialists as compliance partners—they know the pitfalls and can help you navigate them.

3. Use Bonds as a Marketing Tool

Too many entrepreneurs treat bonds as invisible paperwork. In reality, being bonded is a major selling point. Customers often look for the phrase “licensed, insured, and bonded” as shorthand for professionalism and trustworthiness. Don’t hide it—make it prominent on your website, proposals, and even your vehicle signage if you run a service business. One landscaping startup in Colorado reported that including their bonded status in ads increased customer inquiries by nearly 25%—a testament to how much credibility matters.

4. Renew on Time

Most bonds aren’t one-and-done—they require annual renewal. Missing renewal deadlines can invalidate your license, putting your business operations at risk. Beyond regulatory trouble, lapses can also damage your reputation. Imagine explaining to a client that your license isn’t valid because you forgot to renew a bond. The solution: set up reminders in your calendar and designate a team member or accountant to track bond deadlines alongside insurance and tax obligations. Staying proactive ensures continuity.

5. Keep Financial Records Clean

Surety bond premiums are calculated based on risk, and underwriters look closely at your credit history, business finances, and sometimes personal records. Strong financial discipline—keeping debts low, paying bills on time, and maintaining transparent books—signals that your business is trustworthy. Clean records not only lower your premium but also expand your options if you want to scale and take on larger contracts that require higher-value bonds. In other words, good financial hygiene today translates to lower costs and bigger opportunities tomorrow.

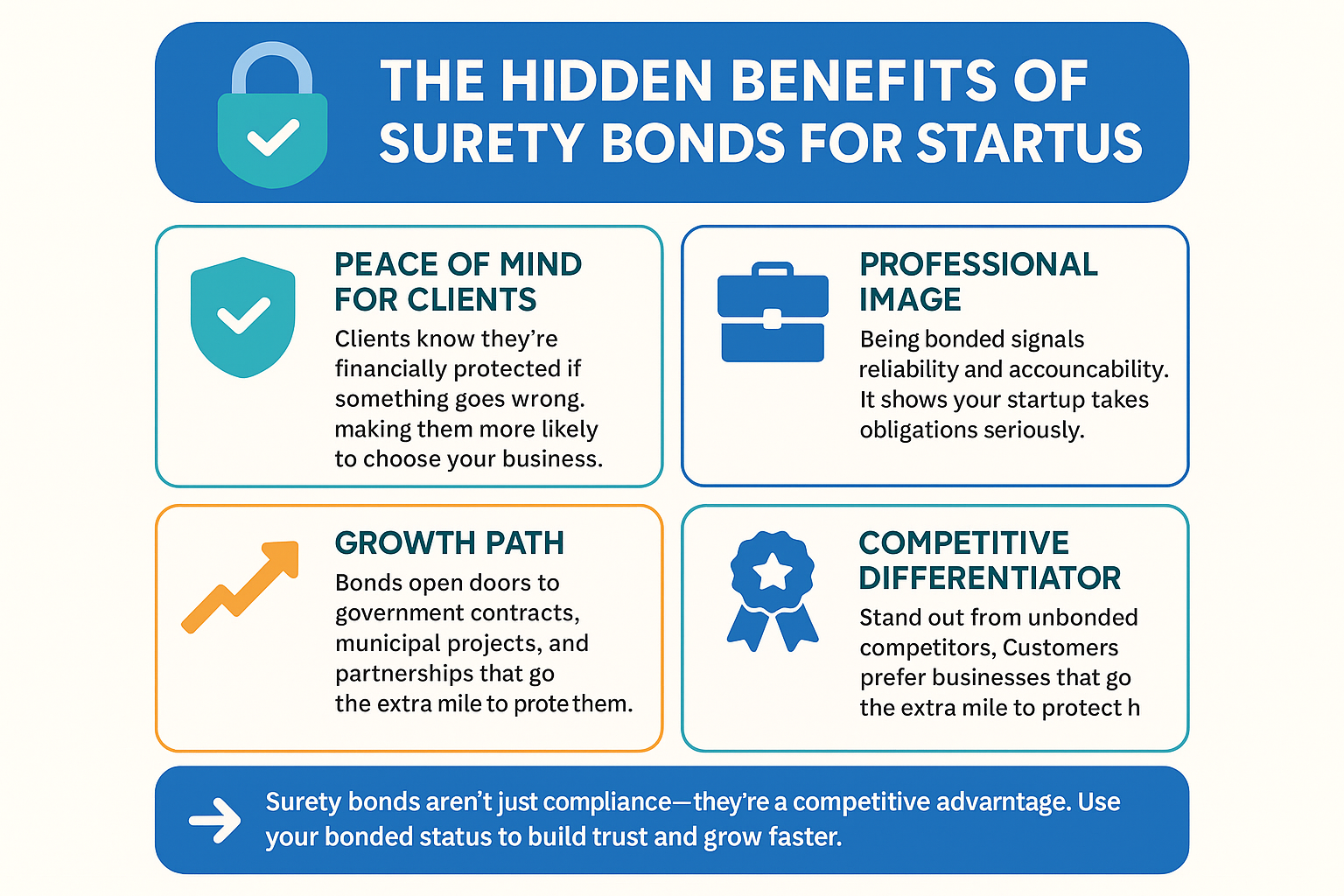

The Hidden Benefits of Surety Bonds

When most entrepreneurs think of surety bonds, they think of compliance. In many industries, being bonded is simply a requirement to get licensed and legally operate. But if you stop there, you miss the bigger picture. Beyond regulatory checkboxes, surety bonds can be one of the most underrated tools to help your startup build trust, elevate its brand, and unlock growth opportunities.

Here are some of the less obvious—but highly valuable—benefits of getting bonded:

1. Peace of Mind for Clients

Trust is everything in business, especially for startups trying to win their first wave of customers. A bond reassures clients that they’re financially protected if something goes wrong. This assurance often tips the scale in your favor when customers are comparing multiple businesses.

Example: A homeowner looking to hire a contractor for a $20,000 kitchen remodel may receive bids from three companies. Two are unbonded, and one advertises itself as “licensed, insured, and bonded.” Even if the bonded contractor’s bid is slightly higher, many customers will choose them for the peace of mind that comes with knowing they won’t be left stranded if the work isn’t completed.

2. Professional Image

First impressions matter, and professionalism often separates successful startups from those that fizzle out. When you can confidently say you are bonded, it signals that you take your responsibilities seriously and have gone the extra mile to meet legal and ethical standards.

It’s the difference between a flyer that simply says “Affordable Plumbing” versus one that reads “Licensed, Insured, and Bonded Plumbing Professionals.” The second version communicates not just affordability, but also reliability and accountability.

Expert Insight from Kevin Kaiser:

“Bonding sends a message to your customers that you’re not just in this for a quick job—you’re here to build a reputation, and you’ve put protections in place for them. That matters.”

3. Growth Path

Surety bonds can also serve as a stepping stone for expansion. Many lucrative opportunities—like government contracts, municipal projects, or corporate vendor agreements—require businesses to be bonded. Without one, you may never even qualify to bid.

Case Study: A small janitorial startup in Illinois began by serving residential clients. When the local school district issued an RFP for cleaning services, bonding was a requirement. By already being bonded, the company was able to apply and ultimately win the contract—tripling its revenue and establishing itself as a serious player in the market.

4. Competitive Differentiator

In crowded markets, being bonded can set you apart from competitors who are not. Customers often don’t understand the technical details of a bond, but they know enough to see it as a safety net. Startups that highlight bonding in their branding and customer conversations position themselves as the safer, smarter choice.

5. Long-Term Stability

Finally, bonding isn’t just about immediate gains—it’s about building long-term stability. Each time you renew your bond successfully and maintain a clean record without claims, you strengthen your reputation with underwriters. This can lower your costs over time and make it easier to qualify for higher-value bonds as your business grows. In essence, bonding creates a virtuous cycle: trust leads to opportunity, which leads to growth, which leads to even more trust.

FAQs About Surety Bonds

Do all startups need surety bonds?

Not every startup is required to be bonded, but many industries—including construction, auto sales, notary services, and healthcare equipment providers—make it a prerequisite for licensing. Even if your industry doesn’t require one, bonding can still give your business a trust boost with customers. Think of it as an investment in credibility. Optional bonds, like fidelity or employee theft bonds, can also protect against internal risks.

How much do surety bonds cost?

The cost of a bond, known as the premium, typically ranges from 1% to 3% of the bond’s total amount. For example, if you need a $10,000 bond, expect to pay between $100 and $300 annually. Your credit score and financial history play a big role in determining the rate. Startups with weaker credit can still get bonded but should expect to pay a higher premium until their business and financial profile strengthens.

What’s the difference between being bonded and being insured?

Insurance protects your business, while bonds protect your customers. If your cleaning crew accidentally breaks a client’s vase, insurance covers it. But if your company fails to finish a project or violates licensing laws, a bond ensures the customer can claim compensation. Both tools are essential but serve different purposes.

Can I get a surety bond if I have bad credit?

Yes, but it may be more expensive. Surety underwriters assess your risk profile, and poor credit means higher risk. Specialized bonding agencies work with high-risk applicants and can still secure a bond, though at higher premiums. The good news: as you pay on time and your financial profile improves, you can refinance your bond at lower rates.

How do customers know I’m bonded?

Once you secure a bond, make it part of your marketing strategy. Display “licensed, insured, and bonded” on your website, contracts, and promotional materials. Don’t assume customers know what it means—educate them in plain language. For instance: “Being bonded means that if we fail to meet our obligations, you’re financially protected.” This clarity builds trust and sets you apart from competitors.

Final Thoughts

For startups, surety bonds aren’t just red tape—they’re a powerful trust-building tool. They open doors to contracts, reassure customers, and safeguard against risks that could otherwise derail your business.

Whether you’re starting a cleaning service, a construction company, or a notary practice, bonding might be the difference between blending in and standing out.

As Kevin Kaiser sums it up:

“Bonding is about credibility. It’s a signal to the world that you take your promises seriously, and you have a safety net in place to protect the people you serve.”

If you’re building a startup, don’t let surety bonds be an afterthought. Instead, treat them as part of your foundation for long-term growth and customer trust.

This article was originally published on November 17, 2009.

Some businesses even use the surety bond as a marketing point to convey a certain image to the public. Advertising the fact that you are bonded will give the customer a sense of trust in you and your company.

Some businesses even use the surety bond as a marketing point to convey a certain image to the public. Advertising the fact that you are bonded will give the customer a sense of trust in you and your company.

Some companies are required to be bonded depending on the industry or trade they may be involved in such as the construction industry.

Some companies are required to be bonded depending on the industry or trade they may be involved in such as the construction industry.

Starting a business is not something you can do overnight. It takes several weeks or even months to get it to the point where you are ready to open for business. You need to do research and I’m not talking just market research but other research as well. In order to be sure that you are operating your business legally, you need to check into local, state, and federal laws regarding your industry. If you want to run your business out of your home, you need to check with the local laws regarding whether or not this is allowed.

Starting a business is not something you can do overnight. It takes several weeks or even months to get it to the point where you are ready to open for business. You need to do research and I’m not talking just market research but other research as well. In order to be sure that you are operating your business legally, you need to check into local, state, and federal laws regarding your industry. If you want to run your business out of your home, you need to check with the local laws regarding whether or not this is allowed.

Thank you for the information that you listed in your article,it is a big help for me to understand what are the requirements of making bonds and how can you be protected when making a bonds negotiation.

Thank you for the information that you listed in your article,it is a big help for me to understand what are the requirements of making bonds and how can you be protected when making a bonds negotiation.

Are surety bond costs just based off of credit? The answer is now Surety bond rates are based off of a multitude of factors. Your credit score does play a big factor in obtaining a rate, but experience, how long you have been in business for and your assets all come into play.

Are surety bond costs just based off of credit? The answer is now Surety bond rates are based off of a multitude of factors. Your credit score does play a big factor in obtaining a rate, but experience, how long you have been in business for and your assets all come into play.

A surety bond may be considered insurance, but unlike insurance a bond does not protect the business it protects the obligee. With insurance you have deductibles, with Bonds there are now deductibles.

A surety bond may be considered insurance, but unlike insurance a bond does not protect the business it protects the obligee. With insurance you have deductibles, with Bonds there are now deductibles.

A surety bond is a promise to pay one party a certain amount if a second party fails to meet some obligation, such as fulfilling the terms of a contract. The surety bond protects the obligee against losses resulting from the principal’s failure to meet the obligation.

A performance bond is a surety bond issued by an insurance company or a bank to guarantee satisfactory completion of a project by a contractor. Performance bonds are commonly used in the construction and development of real property, where an owner or investor may require the developer to assure that contractors or project managers procure such bonds in order to guarantee that the value of the work will not be lost in the case of an unfortunate event.

A surety bond is a promise to pay one party a certain amount if a second party fails to meet some obligation, such as fulfilling the terms of a contract. The surety bond protects the obligee against losses resulting from the principal’s failure to meet the obligation.

A performance bond is a surety bond issued by an insurance company or a bank to guarantee satisfactory completion of a project by a contractor. Performance bonds are commonly used in the construction and development of real property, where an owner or investor may require the developer to assure that contractors or project managers procure such bonds in order to guarantee that the value of the work will not be lost in the case of an unfortunate event.

Hi,

There can be many reasons for this. If you have to be bound with your small business than i suggest you to read this article carefully as it is really informative and useful. There are many consulting industries that are working to guide you properly in such a bounded situations. The web sites like businessstartups.com, alibaba.com are providing nice solutions. It would be really helpful for you.

Best Regards,

William King

Hi,

There can be many reasons for this. If you have to be bound with your small business than i suggest you to read this article carefully as it is really informative and useful. There are many consulting industries that are working to guide you properly in such a bounded situations. The web sites like businessstartups.com, alibaba.com are providing nice solutions. It would be really helpful for you.

Best Regards,

William King

Successful business owners can expect to reap substantial gains from their companies and between the business’s equity and earnings, owning your own business can often be the surest path to financial success and prosperity.

Successful business owners can expect to reap substantial gains from their companies and between the business’s equity and earnings, owning your own business can often be the surest path to financial success and prosperity.

It’s also imperative that your new bonding company have a stellar reputation. After all, you’re trusting them with your finances and, essentially, your reputation should there be a claim on your bond. The bond company should be secure, established, and trustworthy above all else. It’s a good idea to ask other companies in your industry about their chosen bonding company, and to also check with the Better Business Bureau to make sure whichever company you choose has a clean history.

It’s also imperative that your new bonding company have a stellar reputation. After all, you’re trusting them with your finances and, essentially, your reputation should there be a claim on your bond. The bond company should be secure, established, and trustworthy above all else. It’s a good idea to ask other companies in your industry about their chosen bonding company, and to also check with the Better Business Bureau to make sure whichever company you choose has a clean history.

I can imagine that it could be really helpful for a business to be able to have a surety bond. Making sure that they are bonded by a reputable company could be really reassuring. It was interesting to learn about a small business can apply for a surety bond using the same information that would be applied for a loan application.

I can imagine that it could be really helpful for a business to be able to have a surety bond. Making sure that they are bonded by a reputable company could be really reassuring. It was interesting to learn about a small business can apply for a surety bond using the same information that would be applied for a loan application.